Gift of Grain

What farmers are doing is pretty special. Upon delivering grain to the elevator, they now have the opportunity to designate a portion of the load to the Porter County Community Foundation. The Foundation then sells the grain and deposits the proceeds into the Agricultural Community Initiative Fund. Grants are then made from this fund, supporting agriculture educational programs in Porter County.

A gift of grain can be an easy, tax-efficient way to support the community.

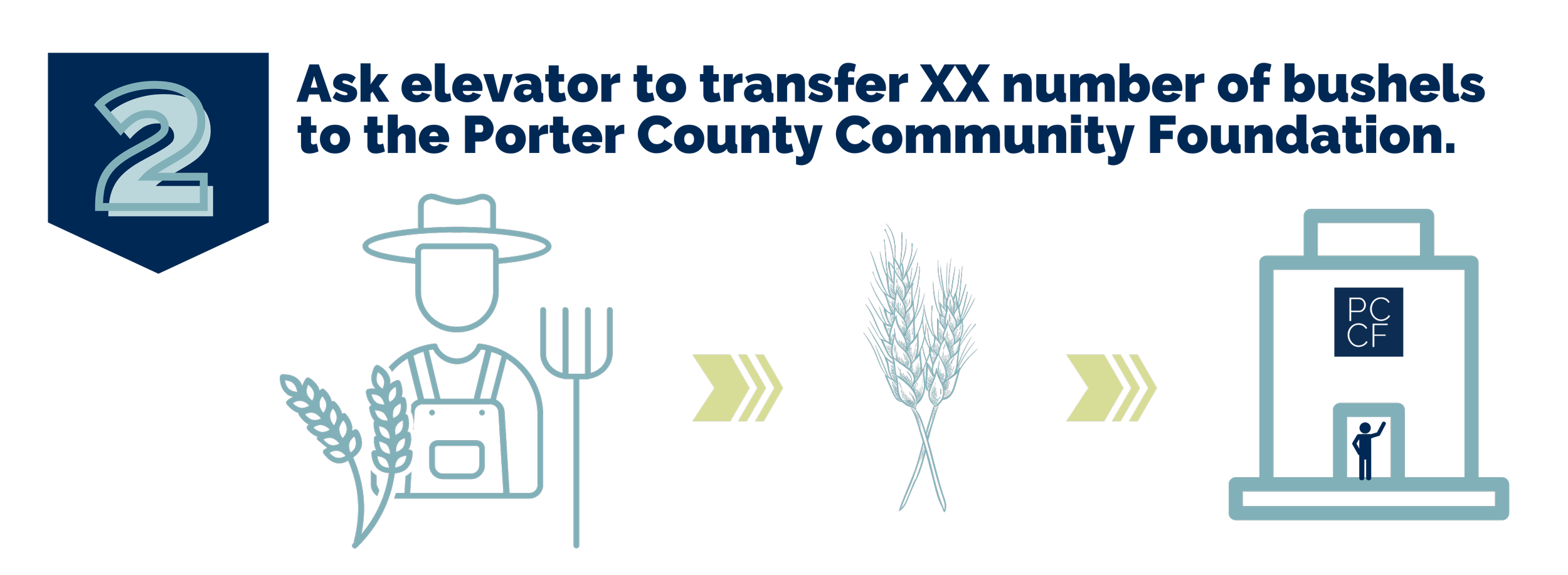

How does it work?

Frequently Asked Questions

How is donating grain better than making a cash donation?

A cash-basis farmer can deduct full production costs on the donated bushels without realizing the taxable income from the sale. This results in savings on Federal, State, County, and Self-employment taxes which would typically amount to more than a standard charitable deduction for a cash gift.

Can a crop-sharing arrangement benefit from this type of donation?

No. Shares of crop are considered rental income and must not be reported as such.

Can I sell the grain, order the proceeds be sent to the Foundation, and still get the same tax benefit?

No. This would be considered a cash donation and would not qualify for the same tax benefits as donating and giving up control of the actual product prior to the sale.

Do I assume any risk between the time I donate the grain and the time the Foundation sells it?

No. The Foundation assumes all risk immediately upon the donation of the product.

Can I store grain on my farm and still make a gift to the Community Foundation?

Yes. You must execute a notarized "Grain Transfer Authorization" form to the Foundation in place of the elevators warehouse receipt.

Can a farm C-corporation benefit in the same way as a sole proprietorship?

C-corporations are treated differently from a tax perspective. Consult your tax professional for guidance in your specific situation.

Will the Gift of Grain count as income in government payments limitation caps?

No. A gift of grain does not count as income in your government payments limitation caps calculation.

Thank You Donors!

Gift of Grain Donors

Mr. Glenn Abbett

Mr. Tyler Abbett

Mr. and Mrs. Cliff Beach

Mr. Chris Birky

Mr. Bryce Birky

Mr. Craig Birky

Mr. Galen Birky

Mr. Greg Birky

Mr. and Mrs. John Birky

Ron and Cheri Birky

Mr. and Mrs. Curt Brust

Mr. and Mrs. Larry Bucher

Mr. and Mrs. Curt Frank

Mr. Joe Cannon

Mr. and Mrs. Jed Chickadaunce

Mr. Carl Peterson

Co-Alliance LLP - Malden Branch

Crop Production Services

Mr. Dave Good

Mr. Ken Good

Mr. and Mrs. Mark Good

Mr. and Mrs. Dale Graeber

Mr. and Mrs. John Gruel

Mr. and Mrs. Ryan Hefner

Mr. and Mrs. Perry Heinold

Mr. Michael Herlitz

Mr. and Mrs. Wayne A. Herlitz

Bill and Karen Higbie

Mr. and Mrs. Marvin King

Mr. Carl Peterson

Jane Maxwell

Mark and Kim Maxwell Family

Mr. Brad Metzger and Mr. Chris Metzger

Mr. and Mrs. Jeffrey R. Overholt

Mrs. Emily Remster

Mr. and Mrs. Dan Roeske

Mr. and Mrs. Paul Rommelmann

Mr. Rob Sands

Mr. Don Schoon

Mr. and Mrs. David Sharp

Mr. Matthew Shurr

Mr. and Mrs. Dennis Steinhilber

Ms. Martha Sharp

Tim and Laura Stoner

Ms. Aimee Tomasek and Mr. Bob Casto